Europe’s industrial economy isn’t booming; it’s recalibrating. Beneath the loud debates on energy transition targets and climate pledges, a quieter story is unfolding, one built on the precision of engineered components like spring-energized seals (SES).

While the global SES market remains modest at about USD 3.5 billion and grows steadily at 5-6 percent a year, Europe’s segment has taken on new strategic weight. The reason is simple but significant: this is where high-performance industries, strict regulatory frameworks, and a push toward localized, innovation-led production converge.

For U.S. manufacturers of advanced sealing systems, understanding this change isn’t optional. It’s the difference between chasing short-term volume and positioning for sustainable value.

While the global SES market remains modest at about USD 3.5 billion and grows steadily at 5-6 percent a year, Europe’s segment has taken on new strategic weight. The reason is simple but significant: this is where high-performance industries, strict regulatory frameworks, and a push toward localized, innovation-led production converge.

For U.S. manufacturers of advanced sealing systems, understanding this change isn’t optional. It’s the difference between chasing short-term volume and positioning for sustainable value.

From Energy to Precision

A quiet reshuffle is happening in the map of demand. Only a few years ago, Europe’s SES consumption revolved around LNG regasification and pipeline infrastructure. That wave has crested. Imports of liquefied natural gas dropped nearly 20 percent in 2024 as new terminals came online, creating excess capacity. Cryogenic sealing for LNG still matters, but it’s no longer a growth engine.

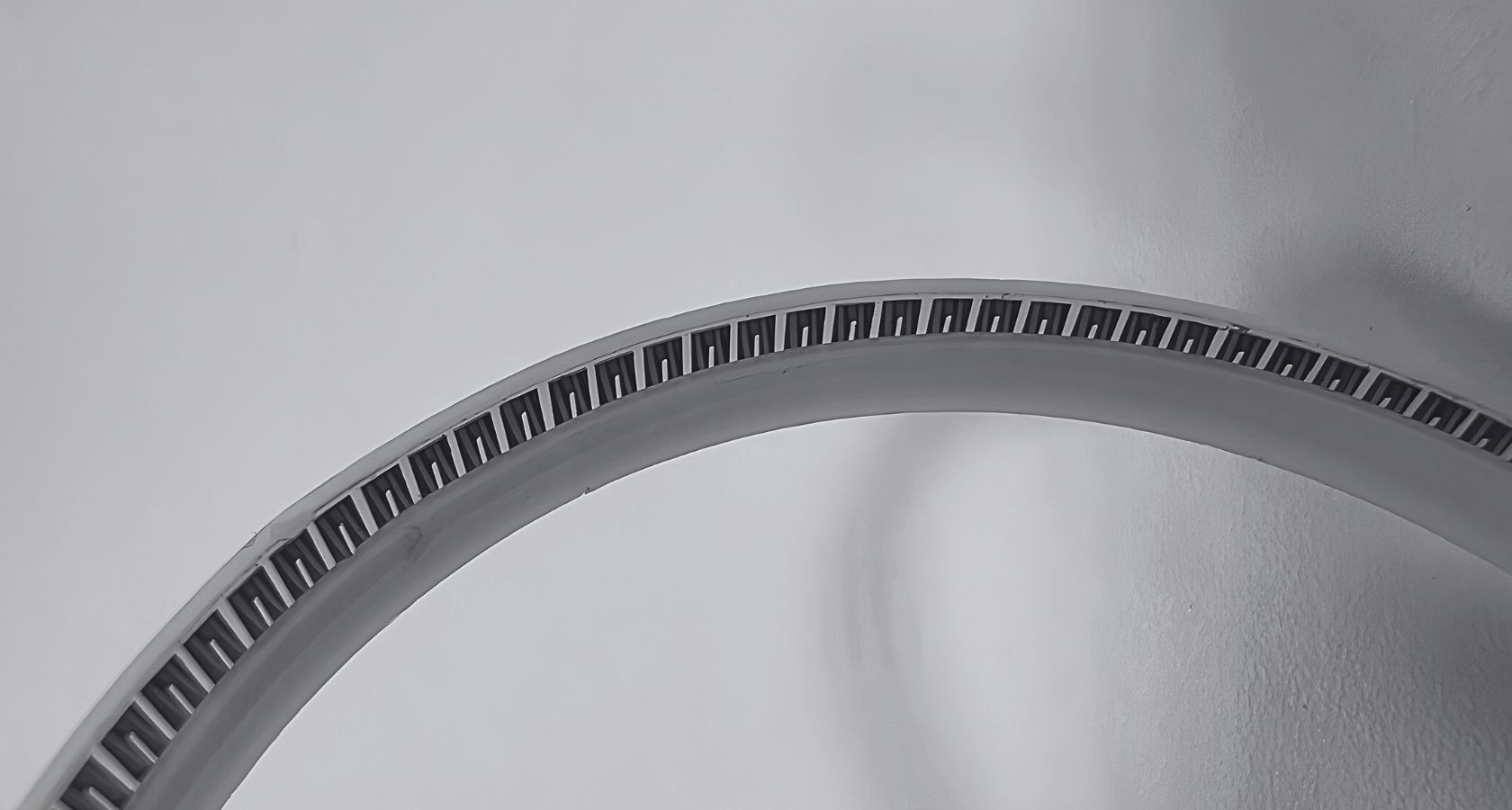

Now, new forces are taking the lead. The EU’s €43 billion Chips Act and the REPowerEU hydrogen initiative are pulling high-spec manufacturing into sharper focus. Semiconductor fabs, hydrogen electrolyzers, and cleanroom assembly lines all require sealing solutions that can survive extremes of temperature, pressure, and chemical exposure. These are the environments where SES technology truly earns its keep. When elastomers distort, a composite PTFE jacket energized by a metallic spring holds geometry, pressure, and trust.

Europe’s manufacturing recovery is uneven, but not random. The sectors that rely most on precision sealing, pharmaceuticals, aerospace, semiconductors, defense, are expanding. Pharma exports grew more than 13 percent in 2024; aerospace production finally exceeded pre-pandemic output; and public investment in hydrogen and chip infrastructure is measured in billions. Every one of these projects demands seals that cannot fail and cannot easily be replaced.

Now, new forces are taking the lead. The EU’s €43 billion Chips Act and the REPowerEU hydrogen initiative are pulling high-spec manufacturing into sharper focus. Semiconductor fabs, hydrogen electrolyzers, and cleanroom assembly lines all require sealing solutions that can survive extremes of temperature, pressure, and chemical exposure. These are the environments where SES technology truly earns its keep. When elastomers distort, a composite PTFE jacket energized by a metallic spring holds geometry, pressure, and trust.

Europe’s manufacturing recovery is uneven, but not random. The sectors that rely most on precision sealing, pharmaceuticals, aerospace, semiconductors, defense, are expanding. Pharma exports grew more than 13 percent in 2024; aerospace production finally exceeded pre-pandemic output; and public investment in hydrogen and chip infrastructure is measured in billions. Every one of these projects demands seals that cannot fail and cannot easily be replaced.

Europe’s industrial shift and new regulations are redefining the spring-energized seal market, revealing fresh opportunities for U.S. manufacturers.

A Market Built on Documentation

Europe’s SES market is defined less by volume than by validation. Buyers in Germany, France, the Netherlands, and Scandinavia rarely debate cents per unit. They scrutinize traceability records, compliance certificates, and lifecycle documentation. Suppliers that can deliver full material genealogy, REACH and RoHS conformity, and wear-cycle data can hold prices that would be unthinkable elsewhere.

This is where many American producers start with an advantage. The U.S. remains ahead in PTFE and PEEK processing, and a good number of U.S. firms already carry aerospace, defense, and medical certifications. Europe’s procurement culture prizes what American engineering already does well — consistency, qualification, and documentation. The challenge isn’t capability. It’s distance.

European buyers rarely wait six weeks for a shipment from Chicago when a certified alternative can arrive from Italy in ten days. To win in Europe, proximity often matters as much as performance.

This is where many American producers start with an advantage. The U.S. remains ahead in PTFE and PEEK processing, and a good number of U.S. firms already carry aerospace, defense, and medical certifications. Europe’s procurement culture prizes what American engineering already does well — consistency, qualification, and documentation. The challenge isn’t capability. It’s distance.

European buyers rarely wait six weeks for a shipment from Chicago when a certified alternative can arrive from Italy in ten days. To win in Europe, proximity often matters as much as performance.

Regulation as Both Risk and Barrier

No market analysis today can ignore regulation, and Europe’s PFAS debate is reshaping the field. The European Chemicals Agency is advancing broad restrictions on per- and polyfluoroalkyl substances, which include PTFE - the backbone of most SES designs.

While “essential use” exemptions are probable, the discussion has already shifted buyer expectations. Procurement teams now request PFAS declarations, evidence of alternative materials in development, and even recycling or end-of-life strategies.

This dynamic cut both ways. Compliance raises costs but also raises the threshold for market entry. Many low-cost Asian exporters, who rely on minimal certification, may find the new environment difficult to navigate. Meanwhile, Western manufacturers offering full traceability could gain a stronger foothold in a less price-driven market.

Some innovators are testing PEEK or polyimide jackets to reduce PTFE exposure. Friction coefficients and extrusion limits differ, but dual qualification, PTFE for aerospace and cryogenic systems, PEEK for life-science and food-grade applications, may prove the most practical path forward.

While “essential use” exemptions are probable, the discussion has already shifted buyer expectations. Procurement teams now request PFAS declarations, evidence of alternative materials in development, and even recycling or end-of-life strategies.

This dynamic cut both ways. Compliance raises costs but also raises the threshold for market entry. Many low-cost Asian exporters, who rely on minimal certification, may find the new environment difficult to navigate. Meanwhile, Western manufacturers offering full traceability could gain a stronger foothold in a less price-driven market.

Some innovators are testing PEEK or polyimide jackets to reduce PTFE exposure. Friction coefficients and extrusion limits differ, but dual qualification, PTFE for aerospace and cryogenic systems, PEEK for life-science and food-grade applications, may prove the most practical path forward.

The Energy Transition’s Uneven Pull

Europe’s energy transformation is uneven - LNG demand wanes, but hydrogen rises. The post-Ukraine war LNG spike is fading, yet hydrogen investment continues to climb. Even if the EU’s goal of 20 million tons of renewable hydrogen by 2030 proves optimistic, achieving half of it would still require enormous sealing capacity for electrolyzers, compressors, and cryogenic systems.

At -423 °F (-253 °C), metals contract, polymers harden, and elastomers surrender. Spring-energized seals, which maintain contact under those conditions, are not optional components - they’re enablers of the hydrogen economy.

At -423 °F (-253 °C), metals contract, polymers harden, and elastomers surrender. Spring-energized seals, which maintain contact under those conditions, are not optional components - they’re enablers of the hydrogen economy.

For U.S. supplier’s familiar with aerospace or cryogenic sealing, this represents a natural adjacency, not a stretch.

The Economics of Trust

What truly underpins Europe’s SES market is trust. Once a seal is validated inside an OEM’s documentation, it tends to stay there. Qualification is slow, replacement slower, and switching costly. This creates stability, and loyalty, that commodity markets rarely offer.

For U.S. exporters, the playbook is clear. Compete on credibility, not price. Build presence, document everything, respond fast. Firms that do can achieve margins 10-20 points above domestic averages.

Of course, the risks remain: PFAS regulation could tighten, hydrogen infrastructure could lag, and currency shifts can undercut profit overnight. But the structural logic endures; in a market where documentation is destiny, the most compliant suppliers often become the most profitable.

For U.S. exporters, the playbook is clear. Compete on credibility, not price. Build presence, document everything, respond fast. Firms that do can achieve margins 10-20 points above domestic averages.

Of course, the risks remain: PFAS regulation could tighten, hydrogen infrastructure could lag, and currency shifts can undercut profit overnight. But the structural logic endures; in a market where documentation is destiny, the most compliant suppliers often become the most profitable.

A Subtle but Significant Opportunity

Europe’s spring-energized seal sector won’t make headlines, but it rewards endurance. It values technical rigor, predictable supply, and relationships built over time. For manufacturers used to short cycles and price wars, this steadiness is refreshing.

Regulation, often viewed as an obstacle, functions here as a moat. It protects the diligent from the opportunistic. Those who understand that compliance can be a competitive advantage, not an administrative chore, will find in Europe a market that quietly compounds value year after year.

Regulation, often viewed as an obstacle, functions here as a moat. It protects the diligent from the opportunistic. Those who understand that compliance can be a competitive advantage, not an administrative chore, will find in Europe a market that quietly compounds value year after year.

Focused First Analytics continues to monitor this market closely, tracking shifts in regulation, technology, and industrial policy, and will keep digging deeper to help clients find where precision becomes an opportunity.

For U.S. manufacturers evaluating their next move, Focused First can assist in answering key questions shaping strategy, whether it's identifying the most effective ways to establish a local presence or partnership in Europe, or preparing for evolving PFAS regulations and demonstrating compliance to European buyers.

We help exporters differentiate themselves from established European and Asian competitors, navigate preferred procurement channels for SES in key markets, and reduce the financial and operational risks associated with currency fluctuations and regulatory changes.

For U.S. manufacturers evaluating their next move, Focused First can assist in answering key questions shaping strategy, whether it's identifying the most effective ways to establish a local presence or partnership in Europe, or preparing for evolving PFAS regulations and demonstrating compliance to European buyers.

We help exporters differentiate themselves from established European and Asian competitors, navigate preferred procurement channels for SES in key markets, and reduce the financial and operational risks associated with currency fluctuations and regulatory changes.